Carbotura

Municipal solid waste, converted to investment-grade raw-material cashflow. A multi-decade securitisation, lending, distribution and trade mandate.

The mandate

We are seeking a single Tier-1 Main Book Holding partner for the multi-decade roll-out of Carbotura. The mandate spans securitisation, balance-sheet retention of risk-retention tranches, M&A advisory, IPO, private-wealth distribution, and physical commodity offtake across the recovered-materials stack.

The full proposal expands each of these into terms-of-engagement, downside cases, sensitivity bands, and counterparty diligence. This page is the cover and reading guide; the proposal PDF and financial model are downloadable from Section 8.

Why we have approached a Tier-1 first

The mandate requires balance-sheet, distribution, structuring depth and a commodities trade book under a single roof. We have identified a small set of institutions that combine these capabilities at the required scale; this brief is delivered to one at a time.

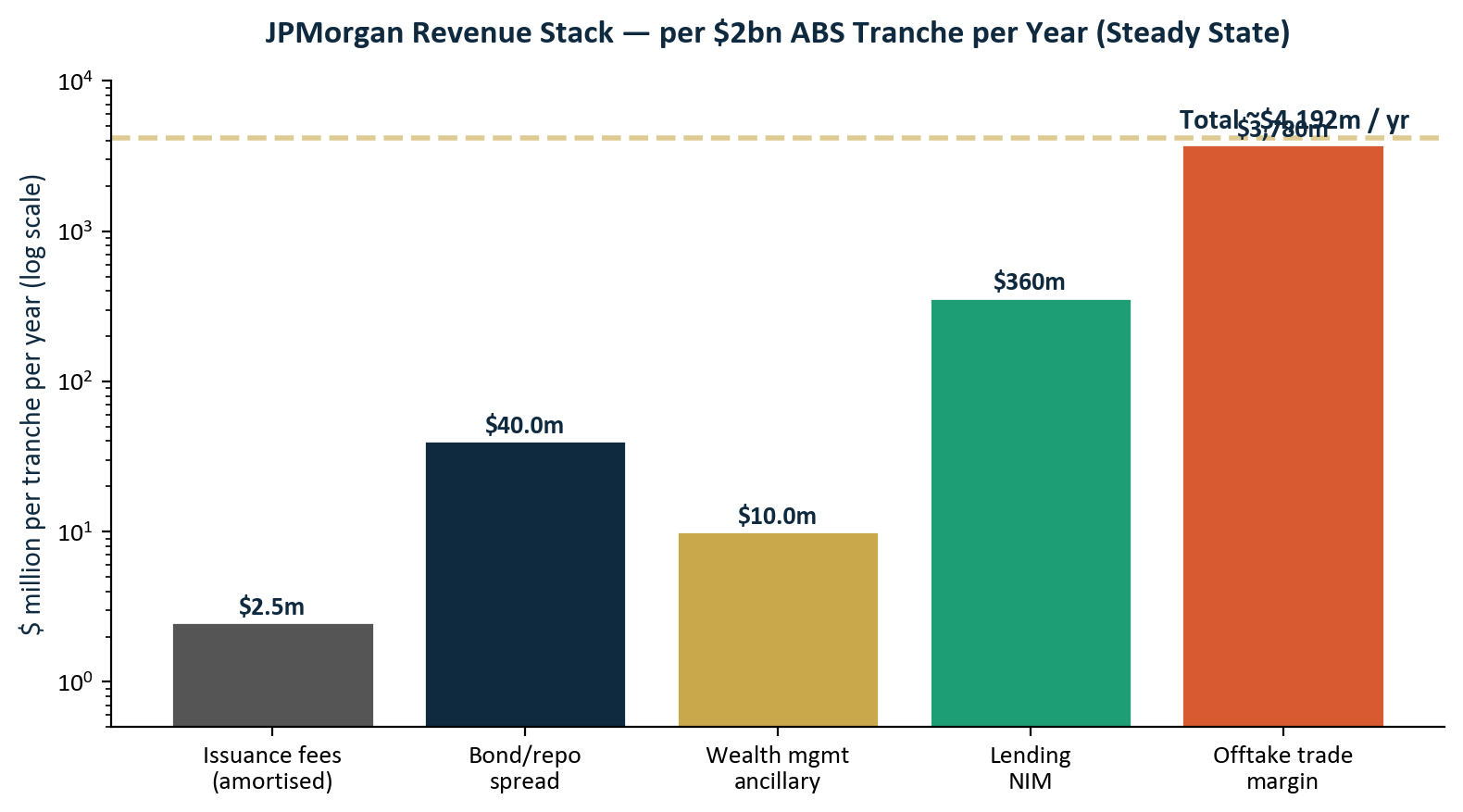

Economic value. Six bank-revenue lines on a normal product set, applied to a multi-decade originated programme. Indicative envelope $15–30m per benchmark tranche per year at steady state, across an estimated 250 tranches over the platform life, plus IPO bookrunner economics, M&A and capital-markets advisory, hedging income, and commodities-trade margin on the recovered-materials offtake.

Brand position. JPMorgan, by anchoring Carbotura, defines a new US ABS sub-asset class — municipal-counterparty-backed circular-manufacturing securities. Rating-agency precedent, distribution book, structuring template and regulatory engagement all migrate from the anchor bank to subsequent issuers in the asset class.

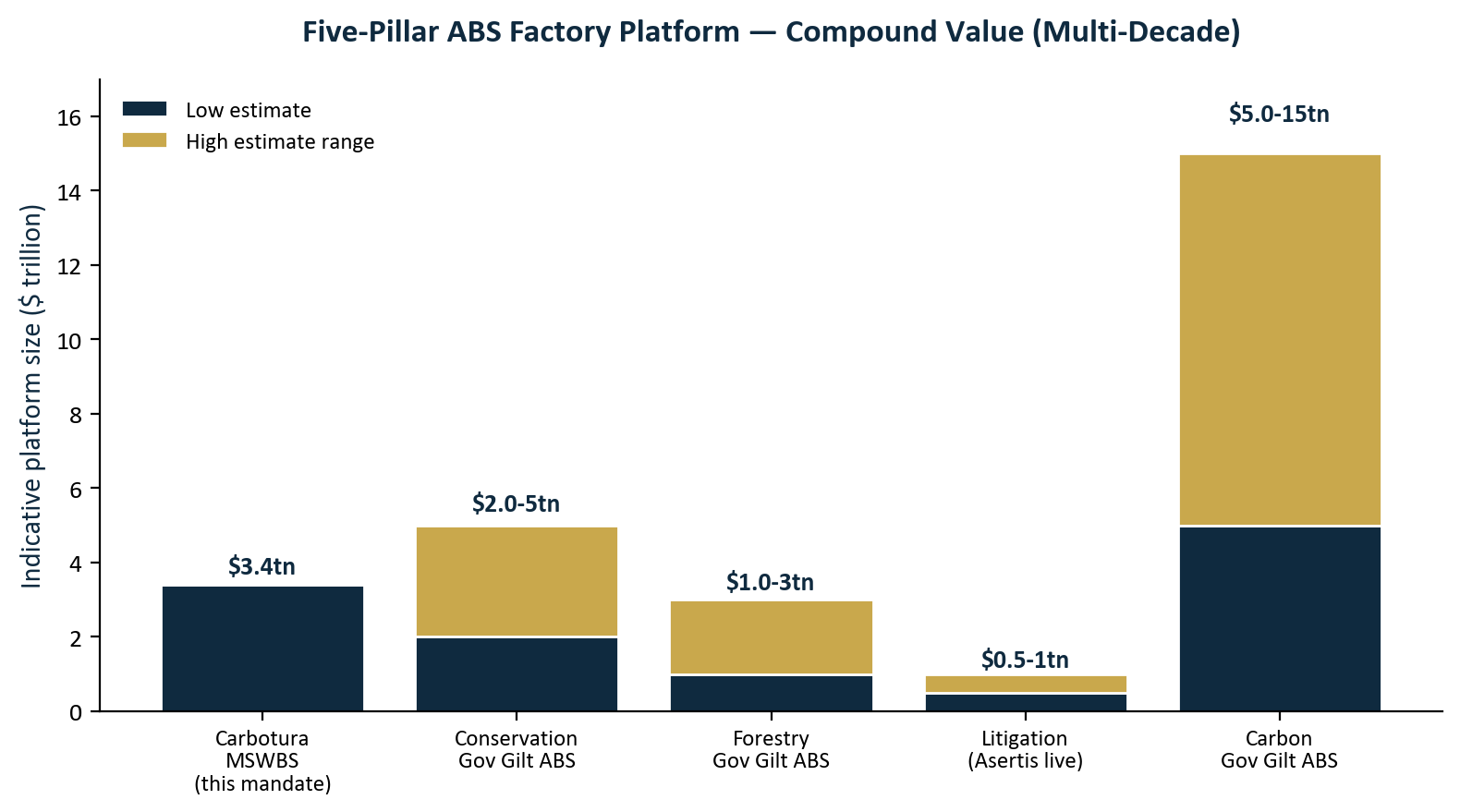

Future business. Carbotura is the MSWBS pillar of the EPC ABS Factory programme. The same architecture is now live across the parallel pillars: CBS (Conservation) and FBS (Forestry) mandate proposals are issued; LBS (Litigation) is operative. The bank that anchors Carbotura is structurally positioned for the parallel mandates — under the same six-line revenue stack and the same Quantitative Growth thesis.

The technology and the seven revenue lines

Carbotura is a tech-enabled circular-manufacturing platform. The proprietary process — Waste-to-Circular Manufacturing (WtCM) — uses the Recyclotron™ Multiphase Microwave Reactor with Microwave Catalytic Reforming, and the RevCon™ Valorization Ladder. EcoGraph™ is the carbon product line. Zero combustion. Zero landfill emissions.

| Revenue line | Indicative scale |

|---|---|

| 1. Total Material Conversion (TMC) fees — tipping-fee equivalent under 30-year Circular Offtake Agreements | $45–150 / t |

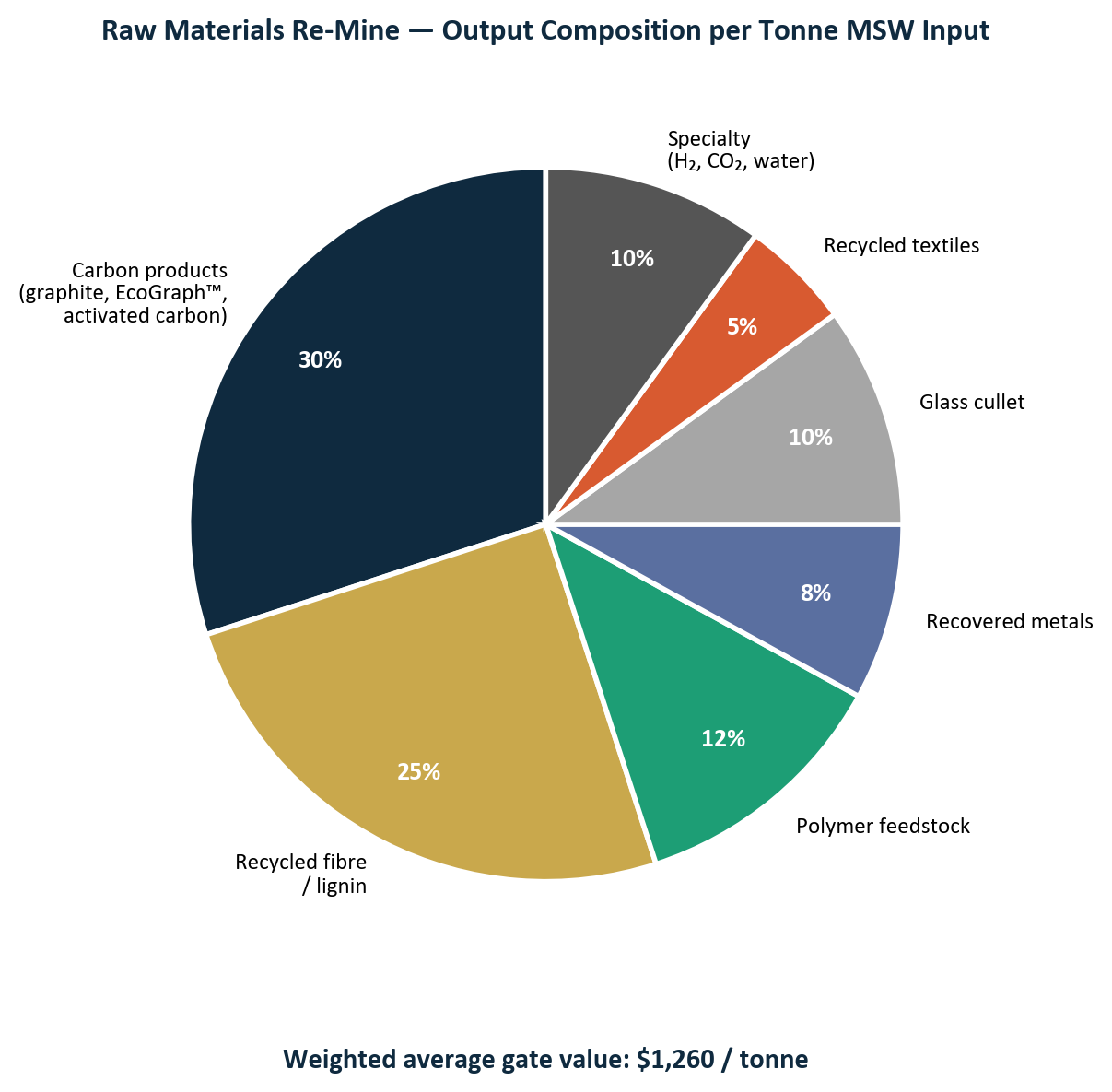

| 2. Strategic materials sales — graphite, EcoGraph™ carbon, recovered metals, fibre, polymer feedstock | $1,260 / t avg |

| 3. Green hydrogen from organic fraction | market + 45V |

| 4. Recovered distilled water | tail-end |

| 5. Food-grade CO2 | ~$200 / t |

| 6. Section 45V hydrogen production tax credit | $0.60–3.00 / kg H2 |

| 7. Section 45Q sequestered-carbon tax credit | $85 / t CO2 |

Output products include synthetic graphite (~$20bn global market, ~70% currently sourced from China) and rare-earth-equivalent recovered materials. Domestic production aligns with bipartisan US critical-minerals policy and is independently eligible for IRA Sections 45V and 45Q.

United States — potential, sourced from public data

The figures below describe the size of the potential opportunity using independent published sources. They are not a forecast of facilities the partnership will build — they describe what the market could absorb at full saturation. Phasing, off-take, permitting and counterparty contracts gate actual deployment.

| Layer | Quantum | Source |

|---|---|---|

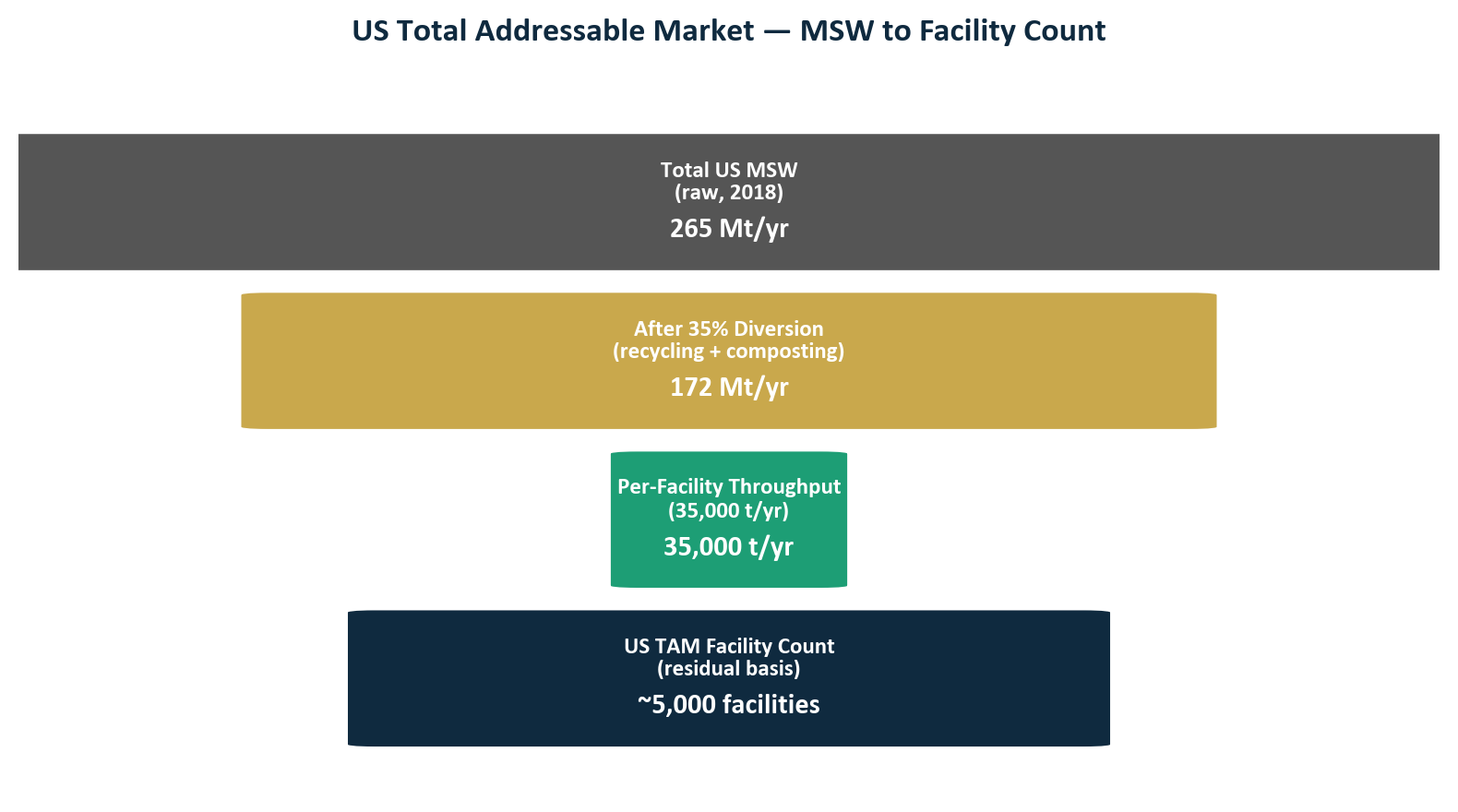

| US MSW generated | ~265 Mt / yr | US EPA, Advancing Sustainable Materials Management: 2018 Tables and Figures |

| Residual after recycling & composting | ~172 Mt / yr | EPA 2018 (calculated as generated less recycled / composted) |

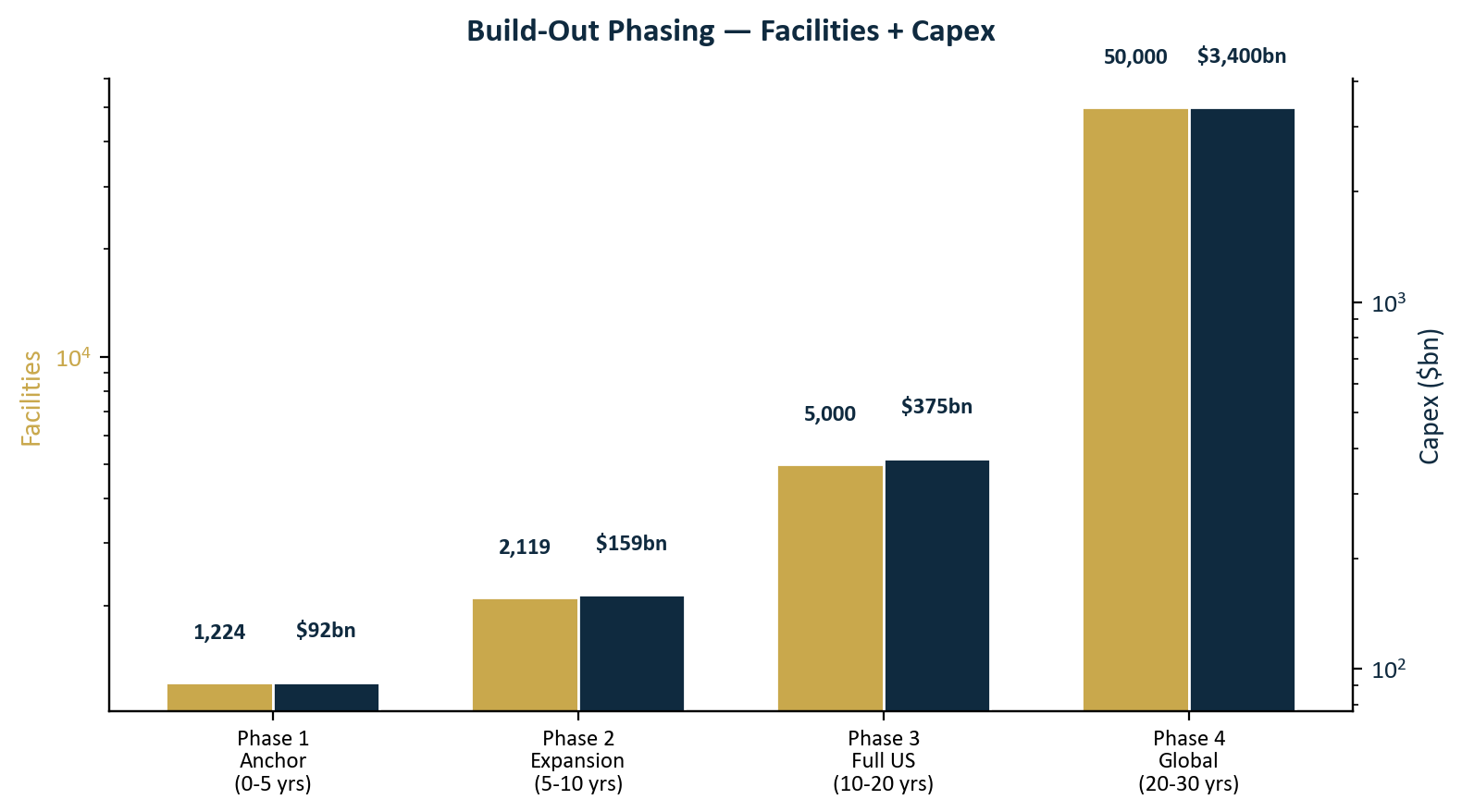

| Implied 100 tpd-equivalent saturation | ~5,000 facilities | Authors’ arithmetic on EPA residual figure ÷ 100 tpd × 365 × 0.94 utilisation |

| State residual concentration | top 10 states ~62% of residual | EREF, Analysis of MSW Management Costs and Practices 2023 |

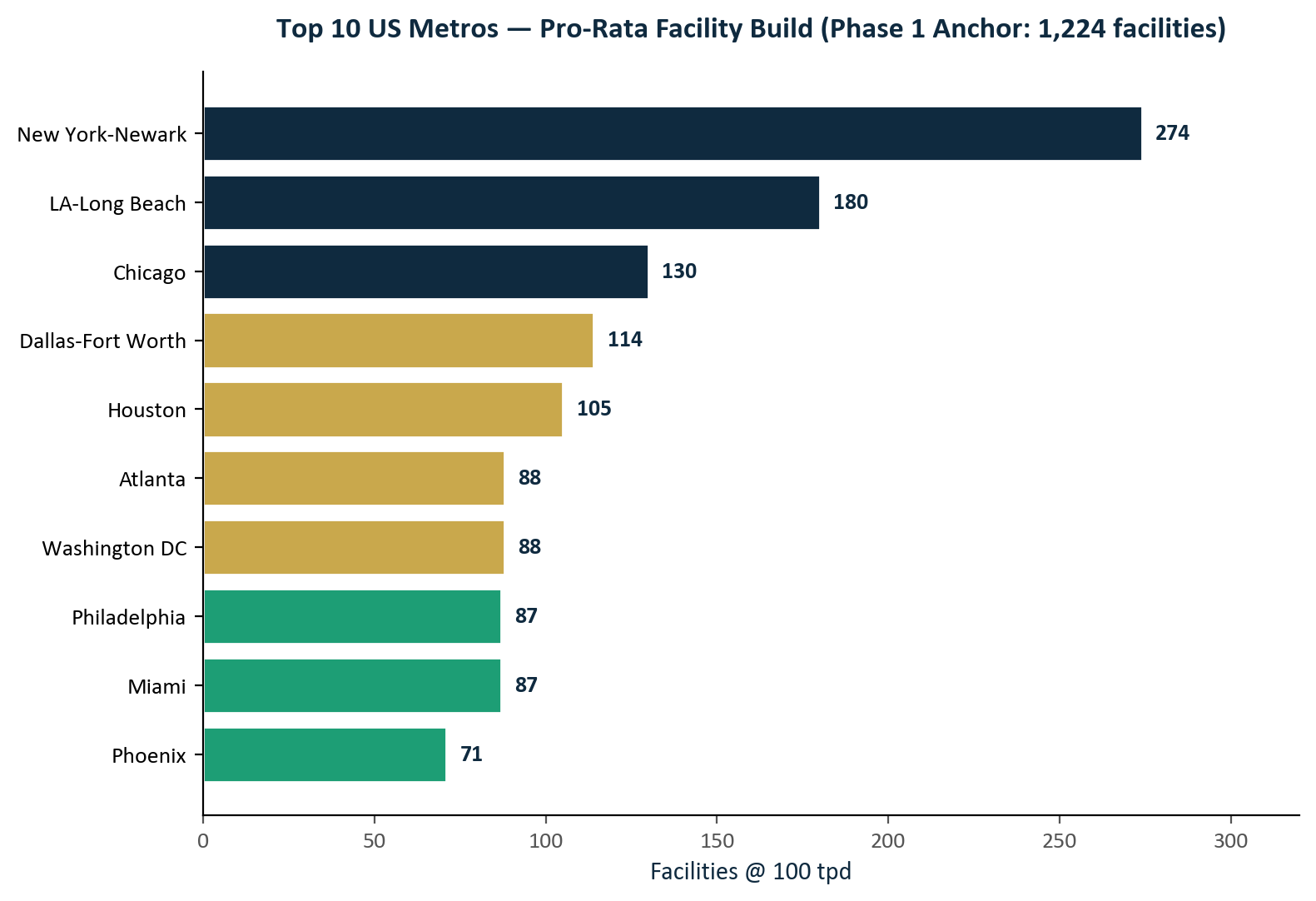

| Top 10 metro coverage | ~43% of US population, 1,224 facility-equivalents | US Census 2023 MSA estimates; SWANA Tipping Fee Survey 2023 for gate-fee bands |

State diversion mandates — California SB 1383, Massachusetts 310 CMR 19.017, Washington SB 5022, New York LL 97 (where adjacent) — create the legal basis for long-dated municipal offtake. The structural feature that makes the asset class new is municipal General Obligation backing of an industrial cashflow.

How the mandate pays the bank

The economics rest on six revenue lines drawn from the bank’s normal product set, applied to a long-duration originated programme. There is no balance-sheet alchemy and no novel regulatory treatment. The figures below are constructed bottom-up from published US bookrunner economics and are stress-disclosed in the financial model.

- Bookrunner / structuring fees on senior issuance Indicative 50–75 bps on $1.5–2.0bn benchmark senior tranches. Per-tranche fee economics: $8–15m.[1]

- Risk-retention and residual-tranche income Under Regulation RR (17 CFR Part 246) the sponsor or arranger retains a 5% economic interest. The retained piece earns the residual / first-loss yield over the deal life and is held to support skin-in-the-game alignment, not to generate Basel HQLA. Indicative steady-state retained-tranche cash yield: 8–14% gross on the retained notional. Important caveat: the retained equity-style strip on a securitisation under SEC-SA / SSFA can attract risk-weights up to 1,250% (dollar-for-dollar capital) per CRR III Art 261 / US Basel III endgame. After CET1 cost of capital absorption the position can be break-even or capital-negative on a risk-adjusted basis; treated here as alignment cost, not standalone income source.[2]

- Construction lending Senior secured construction loans to project SPVs ahead of take-out by the ABS, priced to a spread over the bank’s cost of funds. Specialised-lending risk-weights under CRR III Art 122a / 153(5) and the US Basel III endgame slotting framework span a wide band: 80–100% Strong / stabilised, 100–130% Satisfactory, 190–250% Weak / pre-operational. Pricing accordingly is reflected in the financial model.[3]

- Hedging and ancillary derivatives Interest-rate, FX and commodity hedges on construction draws, off-take pricing, and 45V / 45Q monetisation. Indicative ancillary fee envelope per tranche: $3–6m / yr.

- M&A and capital-markets advisory Equity raises and acquisitions across the 30-year platform build; eventual IPO bookrunner economics. Lumpy but material: indicative IPO economics on a $5–10bn float, $30–50m bookrunner share at standard gross-spread bands.

- Physical and financial commodities trade Recovered-materials offtake intermediation across graphite, recovered metals, polymer feedstock, food-grade CO2, and hydrogen credit monetisation. Trade-margin economics depend on positioning and not modelled here.

The retained risk-retention tranche is not High-Quality Liquid Assets (HQLA) at any level: under LCR Delegated Regulation (EU) 2015/61 Article 7(2) and the US LCR rule (12 CFR Part 50), retained own-issuance securitisations are excluded from HQLA. We do not assume capital relief via significant risk transfer (SRT) under CRR Articles 244–245 on the retained piece. Investor-purchased senior MSWBS paper held by third-party institutions may qualify under LCR Article 13 as Level 2B, subject to structural and concentration tests — that benefit accrues to the buyer, not to the bank as issuer. References to a “multi-trillion lending stack” or undifferentiated Basel III leverage that appeared in earlier drafts have been removed.

Build-out phasing

The programme is phased over 30+ years. Phase 1 is the top-10 metro anchor cohort; Phase 2 extends across the next 50 metros; Phase 3 secondary states; Phase 4 international.

Carbotura within the four-asset-class family

Carbotura is the MSWBS worked example of the wider AiGLe-graded RWA ABS family set out in The Quantitative Growth Thesis. The same securitisation infrastructure that delivers QE-equivalent dilution under MBS works identically when applied to underlying assets that build new productive base. Same machinery. Inverse economic effect.

| Class | Underlying | Issuer / guarantee | Capital treatment |

|---|---|---|---|

| LBS | Litigation portfolios (ATE-floored) | SPV + ATE insurer credit enhancement | Alternative credit |

| CBS | Conservation programmes (perpetual) | Sovereign-issued / sovereign-guaranteed | Basel III HQLA L1 · 0% RW where the security qualifies as a direct sovereign obligation in domestic currency under LCR DR Art 10(1)(c) / CRR Art 114 |

| FBS | Forestry programmes (full-rotation) | Sovereign-issued / sovereign-guaranteed | Basel III HQLA L1 · 0% RW where the security qualifies as a direct sovereign obligation in domestic currency under LCR DR Art 10(1)(c) / CRR Art 114 |

| MSWBS — Carbotura | Industrial waste-to-resource conversion | Variable issuer class — federal / state / municipal-revenue / corporate | HQLA L1 / 0% RW under federal guarantee; otherwise municipal- or corporate-credit RW per issuer class |

Senior-tranche proceeds ($1–2bn benchmark) enter a bankruptcy-remote SPV holding a capital-pool corpus invested in HQLA-eligible instruments under a published Mandate (AiGLe Criteria Paper No. 3). The corpus serves as collateral for construction-loan facilities funding the facility build; programme operations are funded annually from corpus returns; senior coupon is serviced by post-stabilisation operating cashflow; corpus is preserved for the life of the structure. Three structurally distinct credit instruments per issuance — senior MSWBS tranche, construction-loan facility, capital-pool corpus — each priced at the appropriate risk.

Traditional financing forms produce closed transactions. The capital-pool ABS Factory form produces standing financial infrastructure: a graded asset class, a repeatable issuance pipeline, a captive sovereign-wealth-fund corpus, and Basel III-eligible senior tranches. The same underlying transaction generates four structurally distinct revenue streams under the ABS Factory form — project-finance economics on the construction loan, ABS economics on the senior tranche, wealth-management economics on the corpus, and secondary-market / clearing economics on the resulting trading flows — each properly priced, each captured by a single institutional counterparty if the relationship is established at the start of the issuance pipeline.

What sits in mandate, what sits in DD

This document is a mandate proposal. It sets out the structural opportunity, the bank’s economics, the architecture and the heads of terms. It is not a due-diligence pack and does not attempt to substitute for one.

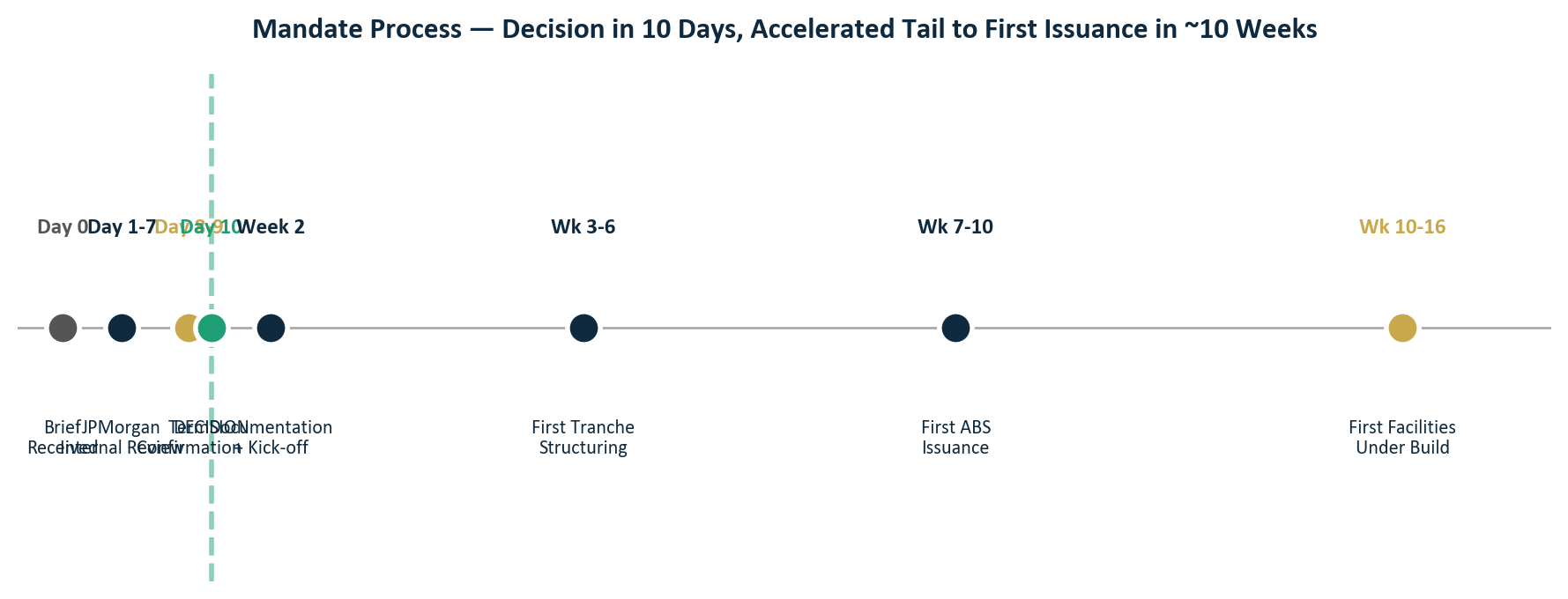

Decision and artefacts

Confirmation of terms is required within 10 days of receipt. The accelerated tail targets first benchmark issuance within 10 weeks. The full proposal, financial model and term-sheet skeleton are below.

Issued under your accepted Confidentiality Undertaking. Each download is logged.

[1] Bookrunner / structuring fee bands derived from Refinitiv ABS league-table data 2022–2024 for senior US ABS issuance ≥ $1bn notional. Actual fee on any specific tranche subject to negotiation, market conditions and competitive process.

[2] Retained risk-retention requirement: 17 CFR Part 246 (US sponsor risk-retention rule); residual tranche cash yield is illustrative and depends on structure, attachment and detachment points, and underlying performance.

[3] Specialised-lending risk-weight bands per Basel III endgame proposal (US OCC / Federal Reserve / FDIC NPR, July 2023) and CRR III (Regulation (EU) 2024/1623). Specific RW depends on supervisory slotting category, project status and rating availability.

Sources cited above: US EPA, Advancing Sustainable Materials Management 2018; EREF, Analysis of MSW Management Costs and Practices 2023; US Census 2023 MSA estimates; SWANA Tipping Fee Survey 2023. Commodity price references: LME, Argus, IHS Markit, ICIS as cited in the proposal annexe.